Economic Overview

As to be expected, the ongoing and dominant economic and market theme remains COVID-19. More so than ever, with COVID present no quarter will be quite like the previous. While Q1 was one of steep decline and pain, Q2 was sharp recovery and euphoria, while in Q3 markets took a slightly more subdued, albeit positive direction. Accommodating monetary and fiscal policy kept the markets happy.

In the US, the economy continued something of a recovery. The Federal Reserve noted it will use average inflation targeting in setting the interest rate, allowing for overshoots in inflation. This means the Fed will allow inflation to move above 2% before it responds. The Fed’s projection path of interest rates indicates it will likely hold rates around 0-0.25% into 2023. The US unemployment rate dropped to 8.4% in August, down from 10.2% in July, while labour force participation also improved. Industrial production rose for the fourth consecutive month in August, but at a much lower rate than earlier in the summer. Similarly, retail sales increased in August, but again at a slower rate and below expectations.

Source: RBA 2020

In the EU, a €750 billion fund was approved to help member states recover from the pandemic. It comprises €390 billion of grants and €360 billion of loans to be distributed among member states. Unfortunately, Covid-19 infections rose rapidly in several countries throughout the quarter, particularly in Spain and France. In response, restrictions to contain the virus were announced. Although these restrictions were localised, opposed to the countrywide restrictions witnessed in the first phase. Various European countries, including Germany, extended furlough schemes designed to support jobs through the crisis. Business activity stalled in September with the flash purchasing manager’s index (PMI) falling to 50.1, down from 51.9 in August. 50 is the level that separates expansion in business activity from contraction.

In the UK, Brexit reared its head again with the potential for a disorderly exit beginning to flare. Not far behind were concerns for a second wave of COVID-19 infections, this saw the localised restrictions imposed in the North, similar to those imposed in some of Europe.

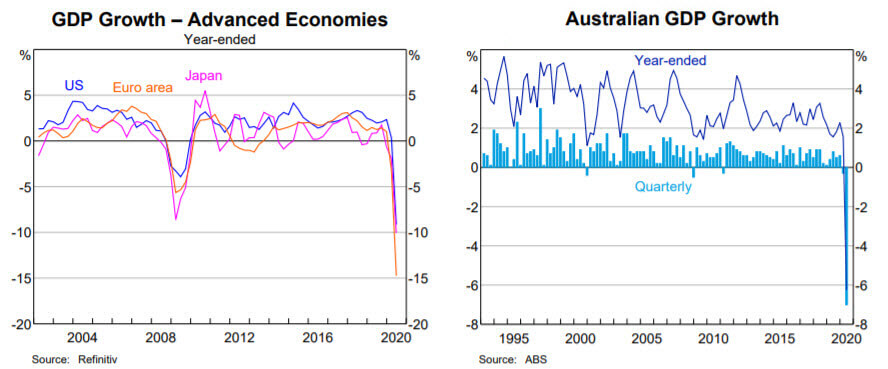

In Japan, the dominant news story was the resignation of Prime Minister Shinzo Abe due to a long-standing health issue. Abe claimed the record as the longest continuous Japanese Prime Minister, then resigned four days later, on August 28. Yoshihide Suga, the Chief Cabinet Secretary, quickly emerged as the frontrunner, being confirmed as PM on September 16. Data for the second quarter showed Japan’s economy recorded a decline for the third consecutive quarter, with the Q2 decline of 7.9% being the largest in GDP data going back to 1955.

In China, economic data signalled ongoing recovery and Q2 corporate earnings results were positive. Q2 GDP growth rebounded to 3.2% year-on-year, after a fall of -6.8% in Q1, and was stronger than expected. However, tensions with the US escalated, including new restrictions on Chinese telecoms company Huawei, and as President Trump signed an executive order to prevent US companies from doing business with TikTok and WeChat. In India, good monsoon rains were supportive, while towards the end of the quarter the government passed agricultural and labour reforms. This was despite a further increase in the number of daily new cases of Covid-19, and as tensions with China on the Himalayan border persisted

In Thailand, the lack of improvement in the tourism sector was a drag on the economic recovery. In Indonesia, Covid-19 cases rose and had an increasing impact, especially in rural areas. As a result, tighter restrictions were brought in for Jakarta.

Back in Australia, the fallout from COVID-19 became evident in headline economic data from Q2. A 7% decline in the three months to June following on from a 0.3% decline in the March quarter, confirming Australia’s first recession since the 1990s. It was also the largest fall in quarterly GDP since records began in 1959. With borders still essentially shut to most overseas visitors for the foreseeable future the government was looking at ways to revive the economy.

One of the more interesting announcements was the Australian government flagging the removal of responsible lending laws, something many commentators flagged was a strange pursuit, given the country has the second-highest household debt in the world. When it came to monetary policy, the RBA left the cash rate at 0.25%, noting in the September release that it expects inflation “between 1 & 1.5% over the next couple of years” and it will not increase the cash rate until progress is made towards full employment and inflation is sustainably between the 2–3%.

Market Overview

Asset Class Returns

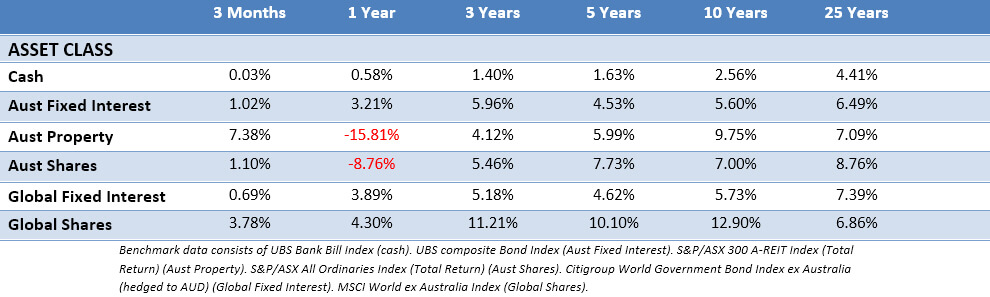

The following outlines the returns across the various asset classes to the 30th September 2020.

Global stocks gained in Q3 but regional performances diverged with Asia and the US outperforming Europe and the UK. Government bond yields were little changed, however, corporate bonds enjoyed a positive quarter. As we noted last quarter government and central bank stimulus are playing their part, while ultra-low rates on cash and bonds means some investors are forced to take additional risk, which may be more supportive of higher stock market valuations.

US stocks gained in Q3 but struggled across September amid a resurgence of Covid-19 cases and political fighting over refreshed fiscal stimulus measures. Worries also grew over the language used regarding a smooth transition of power if President Trump loses his re-election bid. Consumer discretionary areas, such as restaurants and appliances or apparel retailers performed well. Distribution companies were stronger and helped lift the industrials sector, while several airlines still facing headwinds from languishing passenger numbers, offered slightly positive returns. Energy companies remained weak on poor expectations for fuel demand.

Eurozone stocks were basically flat over the quarter. Economic data slowed over the quarter and worries took hold over sharply rising Covid-19 infections in many European countries. The energy and financial sectors saw the largest falls while materials and consumer discretionary advanced, automotive companies also generally fared well.

UK stocks lagged behind other regions during the quarter. This extending their year-to-date underperformance due to the market’s significant exposure to stocks in the oil and financial sectors. The performance was further undermined when UK focused areas of the market were hit in September with the re-imposition of localised restrictions and fears about the impact of these on the UK economy. Pound strength against a weak US dollar weighed on large UK companies with exposure to international markets.

Japanese stocks performed strongly with the Topix Index recording a 5.2% total return. This was despite a gradual strengthening of the yen against the US dollar over the period. Although corporate profits are still under pressure, the earnings season which concluded in early August, brought more positive surprises than many expected.

Asia ex-Japan stocks recorded a strong return in Q3, led by Taiwan, where IT sector stocks underpinned gains. India, South Korea and China all posted double-digit returns and outperformed the MSCI Asia ex-Japan index. Emerging market equities registered a robust return in Q3, aided by optimism towards progress on a Covid-19 vaccine and ongoing economic recovery. US dollar weakness proved supportive. The MSCI Emerging Markets Index increased in value and outperformed the MSCI World.

In Australia, the ASX managed a positive total return, despite some of the largest companies such as the big banks, BHP and CSL finishing slightly lower. Darlings such as Domino’s and buy now pay later company Afterpay continued to power on. The strongest performing sectors were consumer discretionary and information technology. This seemingly still reflects stimulus and early superannuation release sloshing around the economy, while IT is still benefiting from technological changes as workplaces adapt to various COVID related changes. Energy slumped further, as it did elsewhere across the globe.

From an Australian perspective looking globally, unhedged international stocks again trailed their hedged counterparts as the Australian dollar strengthened with the recovery. International small-caps trailed their larger counterparts over the quarter, something that has become a theme for much of the last decade. A similar theme has emerged in the laggard value space. When will these risk premiums return to favour? Unsure, but they can never be ignored. That’s why they’re called risk premiums because they’re not always present. There’s always the next quarter.

Additional material sourced from Schroders.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.